The austerity outlook in the euro area

An interview on the effects of fiscal consolidation on growth and public debt ratios

I did an interview with the French magazine “Alternatives Economiques”, in which I explain my views on the outlook for fiscal policy and macroeconomic developments in Europe based on my recent research. Here is the French version of the interview. In what follows, I provide an English version:

Interviewer: “What lessons can you draw from your analysis of previous fiscal consolidation episodes in the European Union? In comparison, is the adjustment planned for 2025 and beyond a cause for concern?”

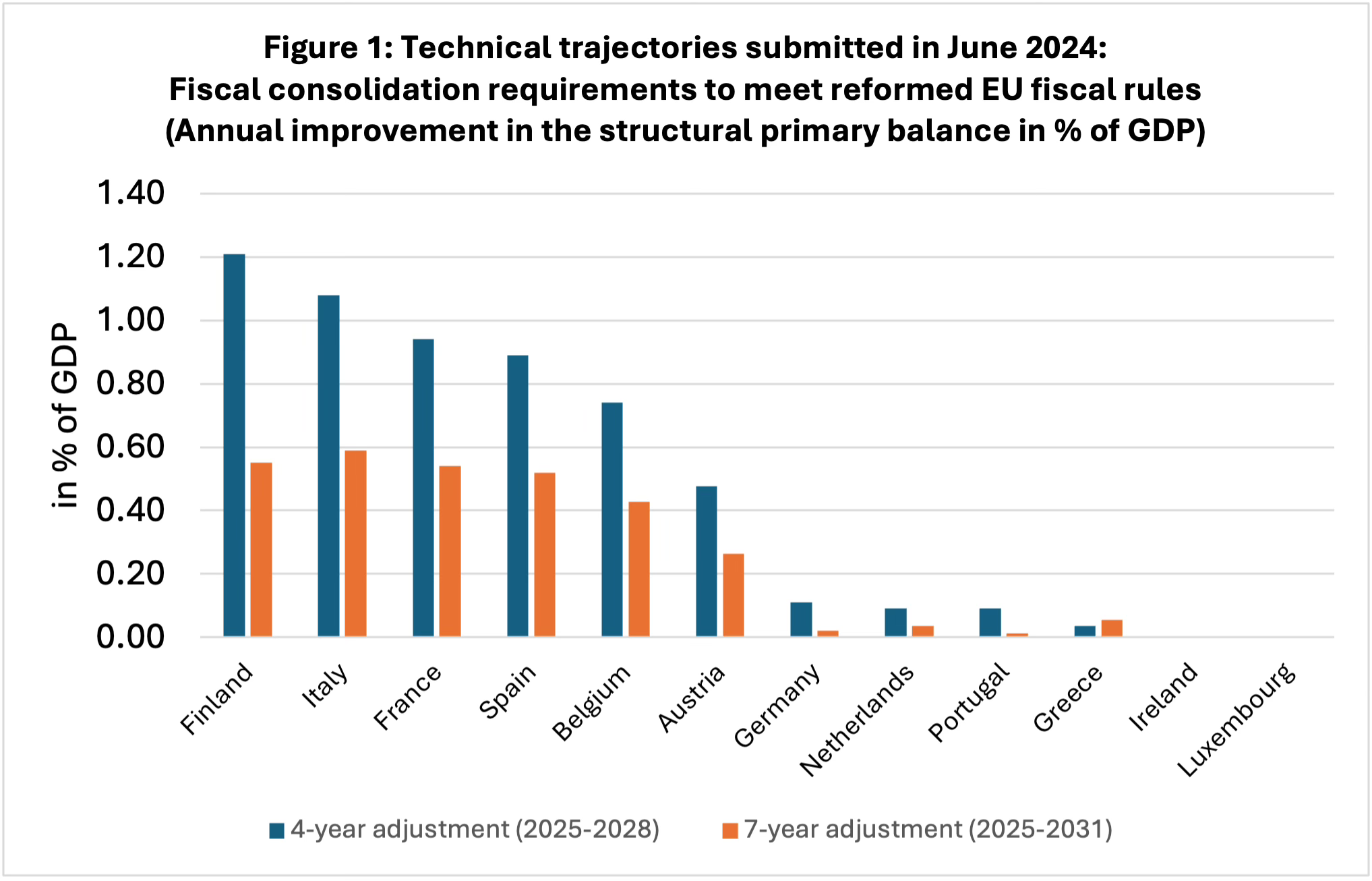

The fiscal consolidation requirements for some member countries are large in historical comparison, including France. The next years are characterised by an austerity outlook: Europe is approaching a multi-year period of simultaneous fiscal contractions in many euro area member countries that represent a large share of the overall euro area economy.

Data: Darvas et al. (2024).

Simultaneous fiscal consolidations across many countries may slow economic growth more than officially expected. Fiscal consolidation during the adjustment period may well lead to economic downturns or at least stagnation, which may trigger a larger-than-expected increase in public debt ratios in the short term, thereby risking a reduction in government approval and an erosion of financial market confidence.

Interviewer: “In your study published in October 2024, you state that the need for fiscal consolidation imposed in the eurozone in the mid-2010s was based on the “incorrect interpretation” that the crisis was fiscal in nature. You also point to a fiscal multiplier estimation error. What is the situation today?”

The key idea of the new framework is that governments just have to show sufficient fiscal discipline to bring public debt ratios down over the medium run. However, if the negative growth effects of fiscal consolidation were to turn out higher than anticipated by the European Commission, public debt ratios may also turn out higher than expected.

Interviewer: “You also demonstrate the contractionary effect of fiscal adjustments on growth, leading to higher public debt ratios. Is fiscal austerity ultimately ineffective, or even counterproductive?”

The overall effect of fiscal consolidation on the economy depends on the timing, the composition and the size of the consolidation. Going for austerity in a downturn and focusing mostly on government spending cuts will give you stronger contractionary effects due to high multipliers. If there are strong and persistent negative effects of austerity on output, the impact on the public debt ratio will indeed be counterproductive, as the debt ratio will tend to be higher in the medium term than it would have been without the fiscal adjustment.

Interviewer: “Then, how can deficits and public debt be reduced?”

If you aim for lower budget deficits in the medium term, you have to think about what needs to happen in different parts of the economy. The greatest potential lies in reducing the household savings surplus through targeted redistribution policies and measures that reduce unemployment and reduce uncertainty, as well as in stimulating credit-financed investments by companies. If you want to have sustainable public finances in the medium and long run, the economy has to be doing well, so that a large number of people have (good) jobs from which they can live and contribute to financing the welfare state by paying taxes and social security contributions. The idea that debt sustainability can be ensured by being more and more restrictive on fiscal policy, without taking the overall economic effects and links to other sectors of the economy into account, is flawed.

Interviewer: “In France, in the current context (economic context, situation in other European countries, global economy, etc.), is it advisable to pursue a policy of budgetary adjustment?”

I think that it is not a good idea to pursue austerity in the current environment. This whole idea is doomed to failure: that the top priority of fiscal policy should be to ensure primary fiscal surpluses via fiscal consolidation at a time when the private sector is not doing well, there are major public investment needs to tackle climate change, when there are major geopolitical uncertainties in the context of wars and trade conflicts. Do policymakers really want to say in ten years: well, we missed the climate targets, social inequality increased, we did not prepare well for the new geopolitical environment, but at least we tried our best to move from primary fiscal deficits to primary surpluses – although we even failed to meet our budgetary targets since the economy did worse than we expected?

One also has to take into account that the academic literature on the political costs of austerity suggests that fiscal adjustments, especially during downturns, lead to a significant increase in extreme parties' vote share, lower voter turnout, and a rise in political polarization. Fiscal consolidations typically reduce government approval, thereby increasing political instability. We should not discuss the economics of fiscal adjustment while ignoring the political economy aspects.

Interviewer: “What room for maneuver does the French government have, within the European budgetary framework, to avoid negative effects on growth, and ultimately public accounts, while carrying out the required budgetary adjustment?”

No matter who will be in government in France in the future, what the government can do is to ask the European Commission to extend the adjustment period from four to up to seven years by submitting a package of investments and reforms. If the European Commission accepts this package, then this will reduce the annual fiscal consolidation requirement substantially. This could at least reduce the negative macroeconomic effects in the short run.

However, the reformed EU fiscal framework does not provide broad-based exemptions for public spending on the green and digital transition. This implies that, if member countries wanted to increase green and digital public spending, they would have to make room for it by restraining other spending items (e.g. social protection, health or education). In sum, the new EU fiscal rules will not enable national governments to promote additional public spending on the green and digital transition on the scale required. Falling behind on the twin transition may then prove to be an economic burden in the long-run, and lower long-term growth would undermine sustainable public finances.

Interviewer: “What is the impact of achieving this through more cuts in government spending or more tax increases?”

It would be counterproductive to achieve the consolidation required to comply with EU fiscal rules mostly through spending cuts. The empirical evidence shows that spending cuts have much stronger negative growths effects than tax measures, particularly during economic downturns.

Data from the International Monetary Fund on fiscal consolidations in developed economies since the 1970s show that governments usually adopt a mix of revenue and expenditure measures when pursuing the goal of reducing the budget deficit. Purely expenditure-side consolidations are rather rare. Moreover, the empirical literature shows that spending cuts have stronger distributional effects at the expense of lower income groups.

The view held in the debate that spending cuts could even have a positive effect on the economy is at odds with the empirical evidence. Even during the euro crisis ten years ago, economists and politicians claimed that spending cuts would boost business and consumer confidence. In fact, the focus on budget cuts in many euro countries exacerbated the downturn, with negative consequences for longer-term debt sustainability.

Of course, there are spending cuts that are less of a burden on the economy than others. However, the multi-year consolidation requirements to comply with EU fiscal rules are so significant that larger groups in the population will inevitably be affected by the spending cuts. Many of the current prominent proposals for government spending cuts would hit low-income earners relatively harder than those with high incomes.

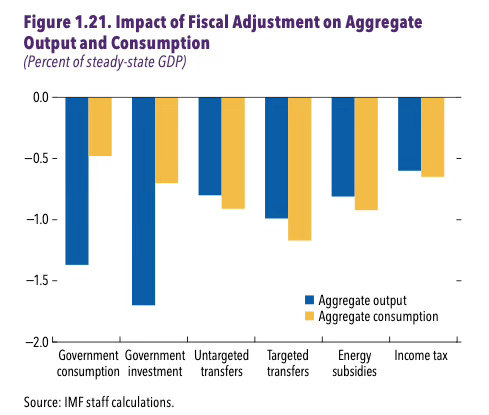

Source: IMF (2024).

The International Monetary Fund also points out in its current research that fiscal consolidation leads to significant declines in economic output and private consumption. Cuts in public investment are particularly detrimental, but a decline in government consumer spending also has a dampening effect. However, the loss of growth is lower when progressive taxes are increased, which hit people with high incomes harder, than when spending is cut.

Interviewer: “A high level of public debt is often thought to reduce growth, which argues in favor of fiscal consolidation when public debt exceeds a certain threshold. However, your quantitative analysis of studies on the subject, published in November 2021, reveals that the causal link between high levels of public debt and lower growth is not so obvious. In the case of France today, do you believe that the level of public debt is reducing economic growth?”

My study provides a quantitative analysis of the whole empirical literature on the impact of public debt levels on economic growth; that’s more than 800 estimates from about 50 studies. Once you properly summarise this literature, there are two main findings: first, the average linear effect of public debt levels on growth cannot be distinguished from zero. Second, there is no evidence for uniform thresholds in the public-debt-to-GDP ratio in all countries beyond which growth falls.

This finding is quite plausible, since there are no strong reasons why there should be a “magic“ threshold in the public debt level beyond which growth slows. The well-known researchers Reinhart and Rogoff claimed this in a famous paper in 2010, and policy-makers used this to argue in favour of spending cuts to bring down public debt. But it was always a chimera – unfortunately a very costly one, since this kind of reasoning has promoted a “one-size-fits-all” austerity approach that has wreaked havoc on the Eurozone during the 2010s.