Cutting corporate taxes is the wrong answer to Germany's growth problems

Cutting corporate taxes is the wrong answer to Germany's growth problems

Germany's finance minister exaggerates positive economic effects of corporate tax cuts

Cutting corporate taxes is the wrong answer to Germany's growth problems

This is a translation of my column published in German business newspaper Handelsblatt.

Last year, Germany's economic growth was weaker than in all other G7 countries. The IMF predicts that this will also be the case in 2024.

Source: Financial Times.

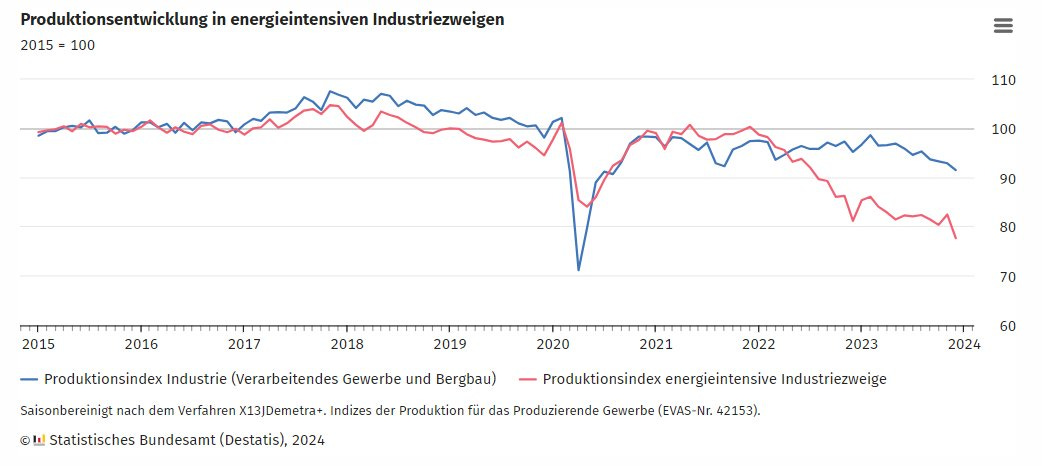

For a long time, Germany was regarded as Europe's industrial powerhouse. However, new data show a broad industrial downturn. Since December 2021, i.e. since the formation of the federal government under Chancellor Scholz, industrial production in manufacturing and mining has fallen by 6%, while production in energy-intensive industries has fallen by as much as 22%.

Source: Destatis.

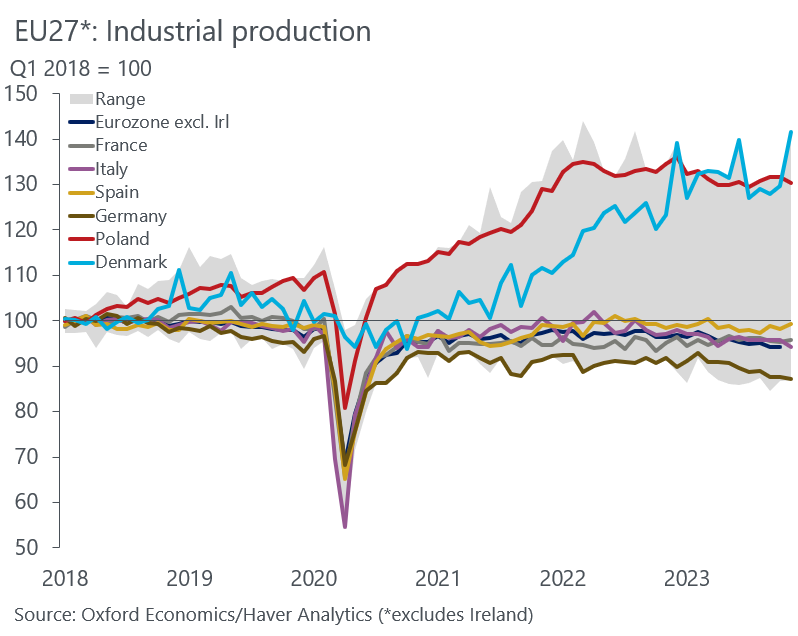

This means that Germany has been one of the worst performers in the EU in terms of industrial production in recent years. The Federal Government's economic policy has not been able to prevent this.

Source: Daniel Kral.

Against this backdrop, the German government has to find an economic policy response to weak growth. Finance Minister Lindner and Economics Minister Habeck want to work on a "dynamization package".

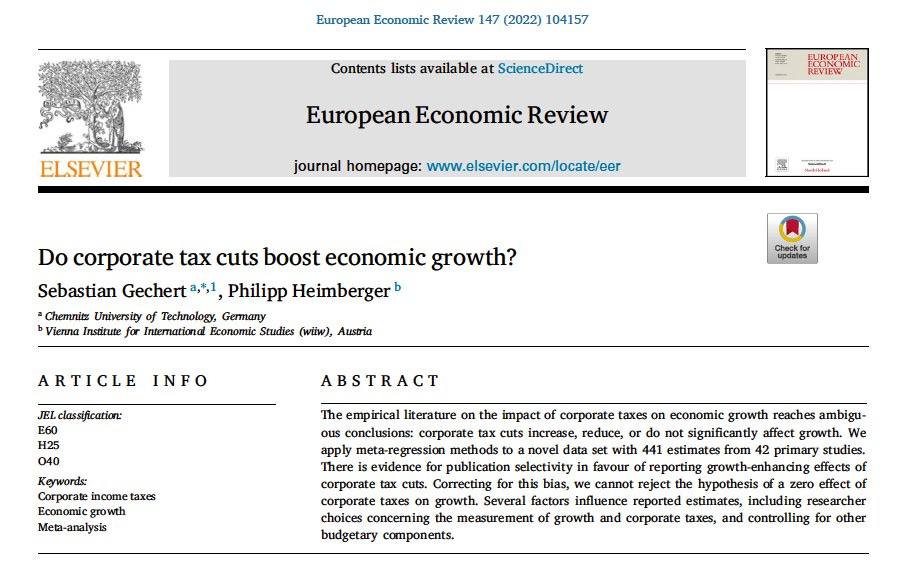

However, the abolition of the solidarity surcharge for companies proposed by Lindner would be the wrong measure. This would mean a blanket reduction in profit tax for companies. The positive growth effects that the finance minister expects from this are exaggerated. Sebastian Gechert and I show in a study that there is little empirical evidence for positive growth effects of such corporate tax cuts.

Source: Heimberger and Gechert (2022).

Especially if government spending is cut elsewhere at the time of the corporate tax cut, weaker growth effects are to be expected. In view of the problems associated with complying with the debt brake and the resulting prospect of government spending cuts, caution is therefore required, especially as a corporate tax cut would lead to a (continued) decline in government revenue.

A loss of tax revenue in turn reduces the provision of public goods such as infrastructure and education. However, the quality of the location for companies and their business prospects are dependent on high-quality public goods.

For German companies to invest more again and for the economy to grow more strongly, the business case for investment must be right. The government would have to make it easier for decision-makers in companies to plan by combining a clear industrial policy strategy with public investment in order to attract further private investment. The turbulence within the federal government surrounding compliance with the debt brake and uncertainties as to whether even long-announced fiscal policy measures in favor of companies can be financed are counterproductive.

Germany's corporate taxation is no longer competitive internationally, it is claimed. Positive effects from across-the-board profit tax cuts are mainly achieved, if at all, by companies relocating to Germany at the expense of other countries. Despite its current weak growth, Germany is Europe's most powerful country both politically and economically. As such, its government should not promote a race-to-the-bottom in corporate taxation that does little for growth.